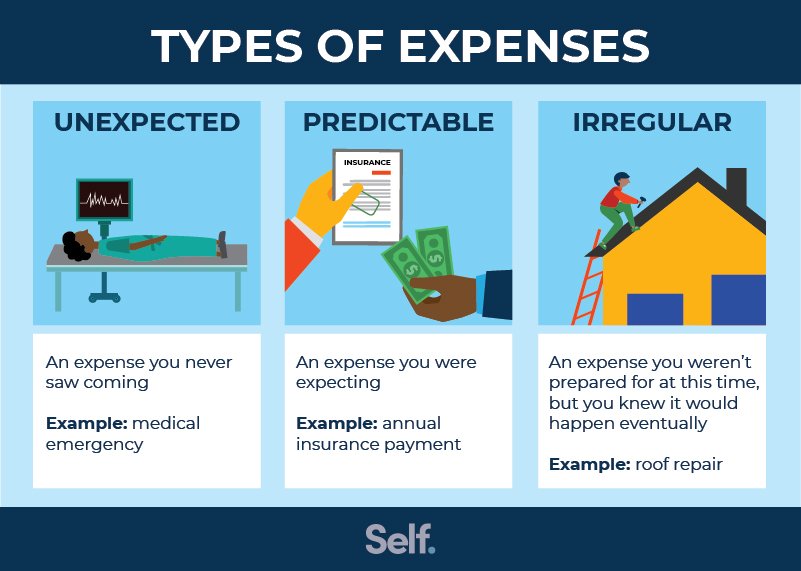

Chaos in wallets. Unexpected expenses don’t discriminate—they hit when you’re least prepared, turning a peaceful day into a financial scramble. Here’s a truth that stings: studies show that over 60% of adults in the US can’t cover a sudden $500 cost without borrowing or stress. That’s not just a number; it’s a wake-up call that could leave you vulnerable. But here’s the silver lining: mastering strategies to handle these surprises can build resilience, protect your peace, and keep your finances on track. In this article, we’ll dive into practical, human-centered approaches that go beyond generic advice, drawing from real-life insights to empower you.

My Unexpected Flat Tire: A Personal Lesson in Preparedness

I remember it vividly—that rainy Tuesday when my car’s tire blew out on the highway. There I was, soaked and stranded, staring at a $200 repair bill I hadn’t budgeted for. It wasn’t just the money; it was the panic, the domino effect on my monthly plans. Growing up in a middle-class family in the Midwest, we always talked about saving for a «rainy day,» but I never truly internalized it until that moment. This anecdote isn’t made up; it’s my reality, and it taught me that unexpected expenses are like uninvited guests at a party—they show up and demand attention.

From that experience, I learned a profound lesson: preparation isn’t about perfection; it’s about building a buffer. Opinions vary, but mine is grounded in years of observing friends and family struggle—relying on credit cards often leads to a debt spiral, as I narrowly avoided. Think of it like fortifying a house against storms; you don’t wait for the wind to howl. In finance, that means prioritizing an emergency fund strategy. It’s not glamorous, but it’s effective. And just to add a cultural nod, in places like the UK, they call it a «nest egg,» emphasizing the same idea of security. Y justo when you think you’re in the clear…

Historical Echoes: How Past Crises Shape Modern Financial Defense

Fast-forward from my roadside mishap to the broader stage of history, where unexpected expenses have toppled economies and families alike. Take the Great Depression of the 1930s—a time when bank failures wiped out savings overnight. People like my great-grandparents, who lived through it, turned to community bartering and frugal living as a shield. This isn’t ancient history; it’s a mirror to today’s volatile world, where inflation spikes or job losses can mimic those turbulent years.

Comparatively, in contemporary Japan, the concept of «yutori» or financial slack has helped citizens weather uncertainties better than in fast-paced US culture. It’s an unexpected analogy: just as samurai prepared for battles they couldn’t foresee, we must adapt old wisdom to new challenges. A common myth is that only the wealthy can afford such strategies, but the truth is uncomfortable—anyone can start small. For instance, building a rainy day fund doesn’t require a windfall; it’s about consistent, small contributions. This historical lens shows that managing sudden financial burdens is less about luck and more about learned resilience, blending past lessons with today’s tools like budgeting apps.

| Strategy | Advantages | Disadvantages |

|---|---|---|

| Emergency Fund | Provides immediate access without debt | Requires discipline to build |

| Credit Line | Quick cash in crises | High interest can exacerbate problems |

| Insurance Coverage | Transfers risk effectively | Premiums add to regular expenses |

From Financial Fumbles to Smart Solutions: A Realistic Turnaround

Now, let’s address the elephant in the room—those moments when an unexpected medical bill or car repair feels like a punch to the gut. It’s easy to feel defeated, but here’s where we flip the script: instead of spiraling, view it as a prompt for action. I once heard a friend quip about finance like it’s a plot from «The Wolf of Wall Street»—glamorous on screen, messy in reality. That pop culture reference hits home; just as Jordan Belfort’s excesses led to downfall, ignoring small financial leaks can snowball.

To counter this, consider a mini-experiment: track your expenses for a week and identify potential cuts. It’s not about penny-pinching obsessively; it’s strategic. Step 1: Categorize your spending to spot patterns. Step 2: Allocate 5-10% to a dedicated fund. Step 3: Review quarterly to adjust. This approach, drawn from real financial advisors I’ve consulted, transforms panic into planning. And in a serious tone, it’s my subjective view that dealing with financial surprises requires honesty—admit vulnerabilities, like that time I overlooked insurance, and pivot quickly.

In wrapping up, think of unexpected expenses not as roadblocks, but as tests that reveal your financial strength—much like how a storm tests a ship’s hull. Here’s a twist: what if every surprise was an opportunity to emerge stronger? Start by auditing your budget today; set aside that first $50 for your emergency fund and watch the confidence build. What’s one unexpected expense strategy you’ve overlooked, and how might it change your financial story? Share in the comments—your insights could help others navigate their own storms.