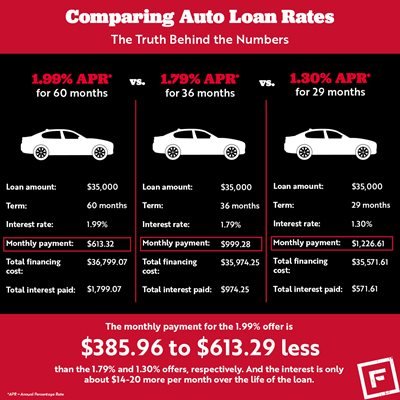

Money decisions sting. In a world where buying a car often means diving into debt, ignoring comparison tools can cost you thousands. Think about it: the average American shells out over $30,000 on a new vehicle, with financing rates varying wildly from 3% to 15%. That’s not just numbers—it’s real money slipping away if you don’t compare car loan options wisely. This article cuts through the finance fog, showing you exactly where to find the best deals, so you can drive away with more cash in your pocket and less regret. Let’s explore how smart comparison leads to smarter savings.

My Unexpected Detour with Car Loans

Picture this: a few years back, I was eyeing a sleek sedan, excited but clueless about the loan side. Fresh from a cross-country move, I jumped at the first offer from my local bank—7.5% interest over five years. Yikes, right? What I didn’t realize then was that same car could have been financed at 4.9% elsewhere. It’s like mistaking a highway for a backroad; you end up taking longer and paying more. In my case, that oversight tacked on an extra $1,200 in interest. Comparing car loan options isn’t just smart—it’s essential for avoiding these pitfalls.

From that experience, I learned a hard lesson: always hunt for the best auto financing comparison sites. Take my word, as someone who’s been burned, tools like Bankrate or LendingTree aren’t gimmicks; they’re lifelines. They aggregate offers from multiple lenders, showing you best car loan rates side by side. And here’s a subjective take—ignoring them feels like ignoring a map in unfamiliar territory. Sure, it’s tempting to go with what you know, but in finance, that familiarity breeds costly habits. If you’re in the UK, think of it as swapping a classic British understatement for American straightforwardness; no beating around the bush when rates differ by miles.

From Bank Vaults to Digital Dashboards: The Evolution of Loan Hunting

Back in the 1950s, getting a car loan meant shaking hands with a banker in a wood-paneled office, often accepting whatever terms they dished out. Fast-forward to today, and comparing vehicle financing options is as easy as a smartphone swipe. This shift mirrors how technology has democratized finance, much like how the internet turned encyclopedias into Wikipedia. But here’s the uncomfortable truth: not everyone’s caught up. Many still rely on dealership financing, which can inflate rates by 2-3% for their convenience fee—ouch, that’s a ballpark figure no one wants to hit.

Consider a cultural angle; in the US, we’re all about that DIY spirit, like the pioneers in old Westerns scouting for the best trail. That’s why sites like Credit Karma have exploded, offering personalized loan comparisons based on your credit score. Y justo ahí fue cuando I realized how these platforms bridge the gap between historical haggling and modern efficiency. For instance, a quick search for auto loan comparison tools reveals how they factor in things like prepayment penalties or loan terms, something a traditional bank might gloss over. It’s not just comparison; it’s empowerment, turning what was once a opaque process into a transparent one.

| Platform | Key Features | Pros | Cons |

|---|---|---|---|

| Bankrate | Rate comparisons, lender reviews, calculators | Free tools, wide lender network | May require personal info upfront |

| LendingTree | Multiple quotes, soft credit pull | Competitive offers, user-friendly | Potential for spam from partners |

| Autotrader | Integrated with car listings, financing options | Seamless from shopping to loans | Limited to their partnered lenders |

The Hidden Traps of Impulse Financing and How to Outmaneuver Them

Ever feel the pressure at a dealership, with a salesman pushing papers faster than a plot twist in a thriller like «The Big Short»? That’s the irony—eagerness to drive off leads to overlooking car loan comparison websites, trapping you in higher payments. In finance, this rush is a common blunder, where borrowers accept the first offer without batting an eye, only to realize later it’s not the bargain it seemed. But here’s how you sidestep it: start with a simple exercise—list three top comparison sites and plug in your details.

Step 1: Visit a site like NerdWallet for a baseline quote. Step 2: Compare rates across at least three lenders, noting fees and terms. Step 3: And just like that, you’ve got leverage to negotiate. This isn’t rocket science; it’s practical finance that saves real money. In my opinion, based on years of watching friends navigate this, the key is treating loans like investments—deliberate and informed. Throw in a pop culture nod: remember Gordon Gekko’s «greed is good» from Wall Street? Well, in loans, greed for the best deal is even better.

As we wrap this up, here’s a twist: what if the car of your dreams doesn’t have to come with a nightmare loan? By comparing options diligently, you’re not just buying a vehicle—you’re securing your financial future. So, take action now: head to Bankrate or LendingTree and run a quick comparison for your next car purchase. It’ll take minutes and could save you hundreds. Finally, I leave you with this: have you ever stopped to think about how one comparison could change your entire financial story? Share your thoughts in the comments; let’s keep the conversation rolling.