Money worries abound, especially when it comes to your child’s future. Did you know that the average cost of a four-year college degree in the U.S. now tops $100,000? That’s a staggering truth that hits hard, turning dreams of education into financial nightmares for many families. But here’s the contradiction: while education opens doors, the path to funding it doesn’t have to be a dead end. In this article, I’ll share practical ideas to fund your child’s education through savvy financial strategies, drawing from real experiences and expert insights. By the end, you’ll have actionable steps to build a solid plan, easing the burden and securing a brighter tomorrow for your kids.

My Unexpected Journey Through Education Expenses

Picture this: back in the early 2000s, I was knee-deep in student loans, staring at a balance that felt like a never-ending mountain. My parents, hardworking folks from a small Midwestern town, had scrimped and saved, but college costs ballooned way beyond their «nest egg.» And that’s when it hit me—preparation is everything. I remember my dad, a factory worker with calloused hands, sitting me down and saying, «Kid, you can’t just hope for the best; you’ve got to plan for it.» His words stuck, teaching me the value of early funding education options.

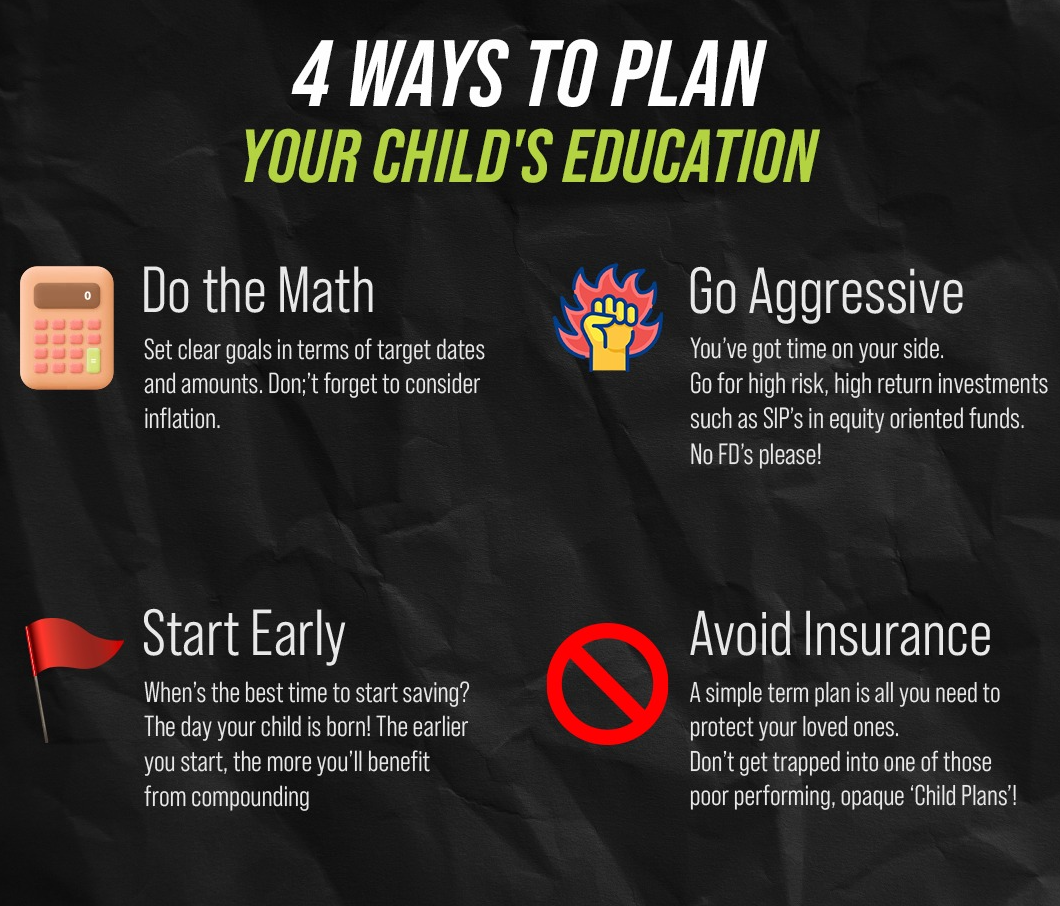

Fast forward, and I’m applying the same lessons as a parent myself. One anecdote that shaped my approach was watching friends navigate saving for college. Take Sarah, a neighbor who started a 529 plan when her daughter was born—it’s like planting a tree that’ll grow into shade for the future. Unlike traditional savings accounts, these tax-advantaged plans let your money compound without the full tax hit. My opinion? It’s a game-changer for middle-class families, offering flexibility for tuition, books, or even room and board. But don’t overlook the emotional side; ignoring it can lead to regrets, as I saw with my uncle who delayed and ended up relying on high-interest loans. That financial planning for kids isn’t just numbers—it’s about peace of mind, too.

Generational Shifts in Funding Strategies

Compare today’s education funding landscape to that of our grandparents, and you’ll see a stark evolution. Back in the 1950s, a college degree cost about $10,000 in today’s dollars—chump change compared to now, when education loans often bury graduates in debt. Historically, families relied on scholarships or family businesses, like the GI Bill that helped post-WWII vets. It’s a cultural reference worth noting: just as soldiers in films like «Saving Private Ryan» fought for a better life, parents today battle financial barriers for their children’s success.

In contrast, modern tools like Roth IRAs for education or state-specific grants offer more tailored options. For instance, while boomers might have leaned on union benefits, millennials are turning to crowdfunding or employer matching programs. This shift highlights a uncomfortable truth: waiting too long can erode your options, much like how inflation erodes savings. I find it ironic that in an era of tech advancements, we’re still grappling with age-old money woes. By weaving in investment options for education, like index funds within a 529, families can outpace inflation—something my generation wishes we’d learned sooner.

A Fresh Take on Scholarships and Grants

Dig deeper, and you’ll uncover that not all funding is about saving; sometimes, it’s about seeking. Unlike the straightforward loans of yesteryear, today’s scholarships demand creativity, from essay contests to niche awards for underrepresented groups.

The Irony of Overlooked Savings Hacks and How to Fix Them

It’s almost laughable—excuse the dry humor—how families obsess over daily lattes while neglecting ways to pay for school. The problem? Procrastination turns into panic, with tuition deadlines looming like a storm cloud. Take it from me: I once thought high-yield savings accounts were too «boring,» only to realize they beat inflation handily. The solution lies in blending discipline with smart choices, like automating transfers to a dedicated education fund. That way, you’re not just saving; you’re building a fortress against future costs.

Consider a simple comparison: a standard savings account versus a 529 plan. Here’s a quick table to break it down, because visuals help clarify education funding strategies:

| Feature | Standard Savings Account | 529 Plan |

|---|---|---|

| Tax Advantages | None | Tax-free growth and withdrawals for qualified expenses |

| Potential Returns | Low interest (e.g., 0.5% APY) | Market-based growth (e.g., 7-10% historically) |

| Flexibility | High, but taxable | State-specific, with penalties for non-educational use |

| Best For | Short-term needs | Long-term funding education goals |

As you can see, a 529 isn’t perfect—there are penalties if misused—but it’s a powerhouse for growth. My subjective take? Pair it with part-time work or merit-based aid for a balanced approach. And just like in the movie «The Big Short,» where spotting trends early pays off, starting these habits now can turn the tide in your favor.

Wrapping Up with a New Perspective

In the end, funding your child’s education isn’t just about dollars; it’s about rewriting your family’s story for the better. Twist that around: what if the real investment is in the lessons learned along the way? So, take this CTA seriously—set up a free consultation with a financial advisor today and outline your first saving for college step. And here’s a reflective question: How will you ensure your child’s opportunities don’t fade due to financial oversight? Share your thoughts in the comments; it’s time to turn talk into action.