Wallets leak silently—that’s the harsh truth many ignore until debt piles up like unwashed dishes. Did you know that over 78% of U.S. households live paycheck to paycheck, according to a recent Federal Reserve survey? It’s a wake-up call in a world where impulsive spending trumps smart saving. But here’s the silver lining: personal finance apps can turn that tide, offering tools to track, budget, and grow your money without breaking the bank. In this tutorial, we’ll dive into navigating these apps, sharing real insights to help you regain control and build lasting financial habits. Stick around, and you’ll walk away with practical steps to make your wallet work harder for you.

That Time Budgeting Bit Me Back

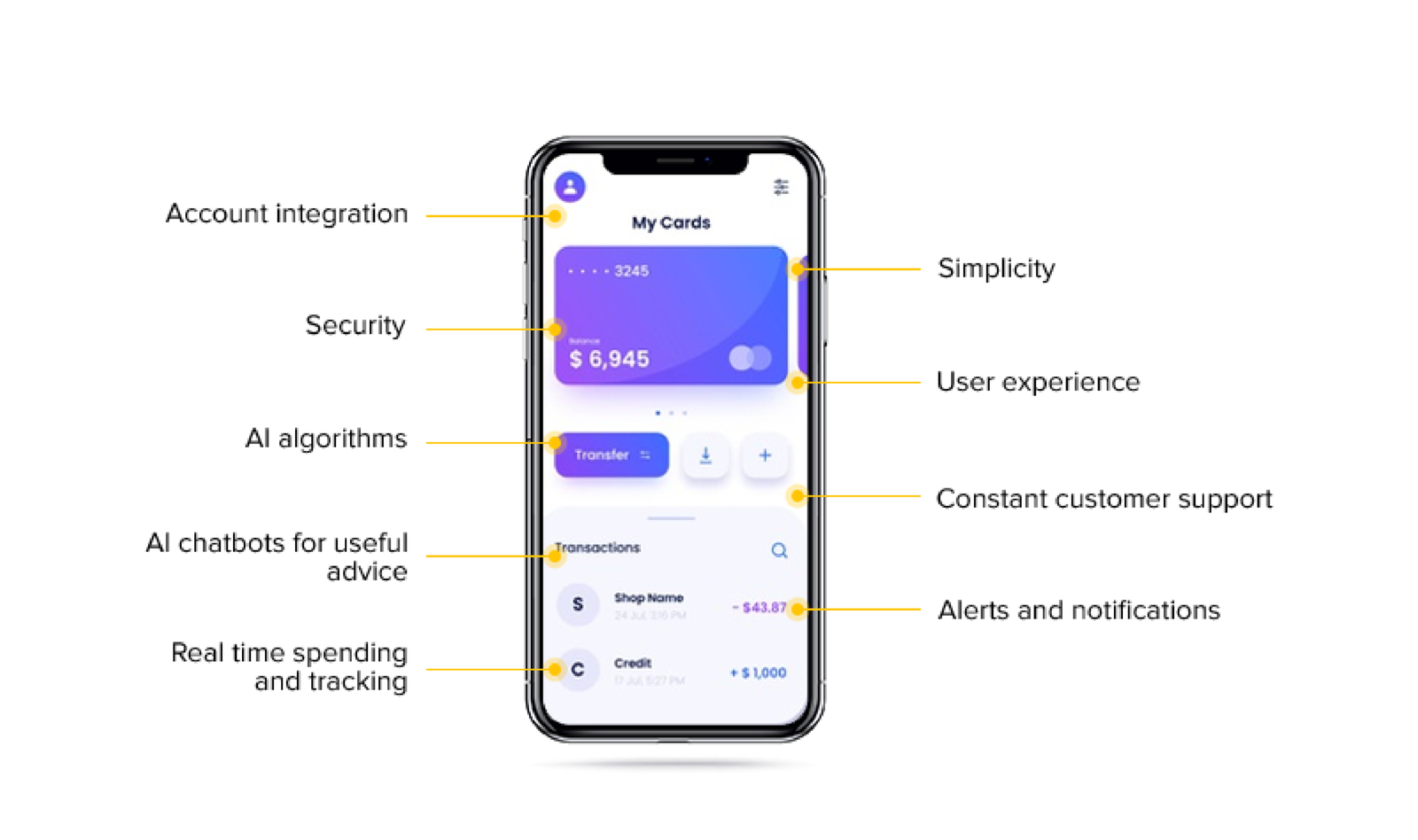

Picture this: a few years ago, I was knee-deep in credit card statements, wondering where my hard-earned cash vanished. It was like chasing shadows—every month, I’d vow to cut back on takeout, yet there I was, ordering pizza again. Enter the Mint app, which I downloaded on a whim after a friend’s nagging. At first, it felt intrusive, like having a nosy roommate tracking every coffee run. But oh, what a revelation. I linked my accounts, and suddenly, categories popped up: groceries, entertainment, that unnecessary subscription I forgot about. Within weeks, I slashed my spending by 20%—no exaggeration. And that’s when it hit me: these apps aren’t just tools; they’re accountability partners in your pocket. Personal finance apps like Mint teach you that small tweaks, like automating savings, can compound into real wealth. It’s not about perfection; it’s about progress, and my slip-ups made me appreciate the nudge notifications even more.

In my opinion, what’s underrated is how these apps humanize finance. They’re not cold spreadsheets; they’re adaptive, learning from your habits to suggest tweaks. Remember, in a culture where «keeping up with the Joneses» often means overspending, apps like these offer a grounded alternative. As an American, I see echoes of the bootstrap mentality—think Ben Franklin’s famous quip, «A penny saved is a penny earned»—reflected in modern budgeting features. If you’re skeptical, imagine me saying, «Hey, reader, you’re thinking it’s too good to be true? Well, try ignoring those expense reports next time and see how that feels.»

From Ledger Books to App Stores: A Timeless Evolution

Fast-forward from the quill-pen days when merchants balanced books by candlelight to today’s swipe-and-track era. It’s a stark contrast—back then, managing personal finances meant poring over handwritten ledgers, a ritual as tedious as watching paint dry. Now, apps like YNAB (You Need A Budget) flip that script, turning complex calculations into intuitive dashboards. Think of it as evolving from a horse-drawn carriage to a self-driving car; both get you places, but one demands less effort and more smarts.

Historically, cultures like the ancient Romans used clay tablets for accounts, embedding finance into daily life much like how mobile banking apps do now. In the U.S., the Great Depression forced families to penny-pinch creatively, a lesson echoed in apps that prioritize emergency funds. But here’s the uncomfortable truth: not all apps are created equal. Some, like Acorns, micro-invest your spare change, blending the old «save your coins» adage with AI smarts. Others, such as PocketGuard, focus on debt reduction, cutting through the noise of modern consumerism. If we compare this to, say, the cultural shift in «The Great Gatsby,» where wealth was flaunted, today’s apps promote stealth wealth—building quietly without the jazz-age excess.

Unmasking the Money Traps and Smart Workarounds

Here’s the irony: even with these high-tech helpers, folks still fall into pits, like oversharing data or ignoring alerts until it’s too late. Take security breaches—remember that Equifax hack a few years back? It shook me, making me double-check app permissions like a paranoid detective. The problem? Many users treat these apps as set-it-and-forget-it, but without regular reviews, you’re leaving money on the table. And just there, expenses creep up unnoticed.

To counter this, let’s break it down practically. First, choose an app that fits your style—say, for beginners, apps like Goodbudget use the envelope system, mimicking old-school cash allocation in a digital wrap. Second, integrate it with your goals; for instance, if debt’s your demon, apps like Debt Snowball track payments with motivational charts. Third, and this is key, review weekly—it’s like checking under the hood of your car before a road trip.

| App | Key Feature | Pros | Cons |

|---|---|---|---|

| Mint | Automated budgeting | Free, user-friendly, integrates multiple accounts | Ads can be intrusive |

| YNAB | Zero-based budgeting | Teaches discipline, detailed reports | Paid subscription |

| Acorns | Micro-investing | Easy to start, rounds up purchases | Fees add up for small investors |

This comparison shows how personal finance apps for budgeting vary, helping you pick without buyer’s remorse. In a serious tone, it’s about arming yourself against financial fatigue—after all, who needs another «Wolf of Wall Street» meltdown when you can stay ahead with data?

A Quick Experiment for You

Why not try this: download one app today and track just one category for a week. You’ll see patterns emerge, like I did, and maybe even laugh at your own spending quirks.

Wrapping this up with a twist: while apps are powerful, they’re only as good as the habits you build around them. True financial freedom? It’s not in the tech; it’s in you. So, take action—pick an app from our chat and set up your first budget right now. And here’s a reflective question: what’s one financial habit you’ve been putting off, and how could an app change that? Share in the comments; let’s keep the conversation real.