Wealth hides quietly. It’s not the flashy cars or the Instagram-worthy vacations; it’s that silent number lurking in your bank statements and debt ledgers. Yet, here’s the contradiction: in a world obsessed with money, most people stumble when asked to pinpoint their exact net worth. According to a recent survey by the Federal Reserve, nearly 40% of Americans have no idea how to accurately calculate it. This ignorance isn’t just harmless—it’s a barrier to smart financial decisions, leaving you vulnerable to poor investments or overlooked savings. But don’t worry; by the end of this guide, you’ll grasp a simple method to calculate your net worth, empowering you to take control of your financial future and make choices that align with your goals. Let’s dive in, shall we?

My Unexpected Financial Awakening

I remember the day I first tallied up my net worth like it was yesterday—it hit me harder than a plot twist in a Martin Scorsese film, you know, like in ‘The Wolf of Wall Street’ where the facade crumbles. Back in my early thirties, I was coasting through life, thinking my steady job and modest savings meant I was set. But when I sat down one rainy evening in Chicago—yes, that windy city where the cold makes you reflect—I realized I hadn’t a clue about my true financial standing. I listed out my assets: the apartment I owned, my retirement account, even that old car still running. Then came the liabilities: student loans that wouldn’t quit and credit card debt from impulse buys. Subtracting them revealed a number that was, frankly, underwhelming. And that’s when I realized… my financial security was a myth.

This personal anecdote isn’t just filler; it’s a lesson in humility. **Net worth calculation** starts with brutal honesty. In my opinion, ignoring this step is like driving without a map—you might get somewhere, but you’ll probably hit dead ends. For those in the U.S., where consumer debt often sneaks up like an uninvited guest at a barbecue, this exercise forces you to confront realities. Think of it as a financial mirror, reflecting not just numbers, but your life’s priorities. By sharing this, I’m not boasting; I’m urging you to do the same, using everyday tools like a spreadsheet or an app, to build a foundation for lasting stability.

Empire Builders and Everyday Balances: A Historical Lens

Picture this: ancient Roman emperors meticulously tracking their vast estates and debts, much like how we juggle mortgages and stocks today. It’s a comparison that might seem far-fetched, but bear with me—history shows that understanding net worth isn’t a modern invention. In fact, the concept dates back to medieval ledgers, where merchants in bustling trade hubs like Venice calculated their fortunes to avoid ruin. Fast-forward to now, and it’s no different; your net worth is your personal empire, a snapshot of assets minus liabilities that reveals your economic standing.

Here’s where it gets interesting: in American culture, we often romanticize rags-to-riches stories, but the truth is uncomfortable—many overlook simple **net worth formulas** because they seem tedious. For instance, comparing the net worth of a historical figure like John D. Rockefeller, who amassed billions in today’s terms through oil, to your own might highlight disparities, but it also underscores a universal truth. As I see it, every dollar you own or owe tells a story of choices made. Don’t let your finances go south, as the saying goes; instead, embrace this historical perspective to appreciate how a straightforward calculation—assets like cash and investments minus liabilities like loans—can prevent you from repeating past mistakes. It’s not about being a tycoon; it’s about being informed, especially in a country where economic mobility is as unpredictable as a New York stock exchange dip.

| Method | Advantages | Disadvantages |

|---|---|---|

| Manual Spreadsheet (e.g., Excel) | Customizable and detailed; helps track changes over time | Takes time and requires discipline |

| Financial Apps (e.g., Mint or Personal Capital) | Automated updates and visualizations; user-friendly for beginners | Relies on accurate input and may have subscription fees |

| Professional Advisor Consultation | Expert insights and tailored advice | Can be costly, breaking the bank for some |

The Overlooked Dangers and Your Path to Clarity

Ever wondered why so many folks bury their heads in the sand when it comes to finances? It’s ironic, really—while we chase promotions and side hustles, we sidestep the basic act of calculating net worth, thinking it’ll sort itself out. But here’s a disruptive question: what if that avoidance is costing you thousands in missed opportunities? Take my earlier experience; by not facing the numbers, I delayed paying off high-interest debt, which snowballed like an unchecked snowball in a Colorado winter. The solution? A step-by-step approach that’s as straightforward as brewing coffee.

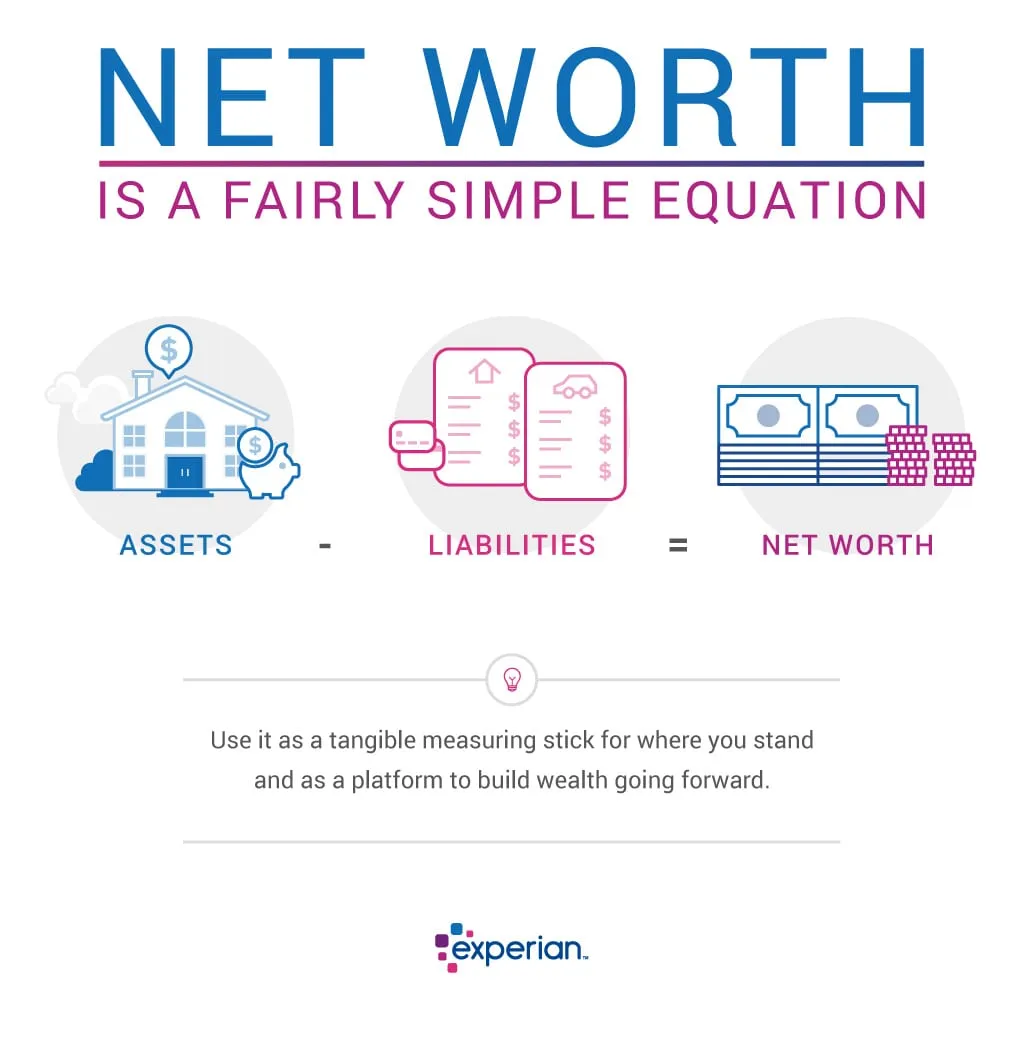

First, gather your assets: cash in the bank, value of your home, retirement funds—anything you own that holds worth. Number two, tally your liabilities: mortgages, credit cards, loans that demand repayment. Three, subtract the latter from the former to get your net worth. It’s that simple, yet profound. I firmly believe this process, often called the **simple net worth formula**, acts as a wake-up call, revealing hidden vulnerabilities. For U.S. readers, remember how tax seasons expose financial gaps? This is your proactive version. And just like in a tense episode of «Billions,» where characters dissect every asset, you too can turn the tables on uncertainty. No need for fancy tools; a notebook works fine, though apps add convenience.

In wrapping this up, think of your net worth not as a final verdict, but as a starting point for growth—that’s the twist. While we’ve crunched numbers, the real power lies in what you do next. So, take action: pull out your financial statements right now and calculate your net worth using the steps above. How will this newfound awareness reshape your spending habits and long-term plans? I’d love to hear your thoughts in the comments—let’s make finance personal again.