Debt sneaking in? It’s a silent thief, eroding your wallet while you scroll through endless online deals. Picture this: the average American household shells out over $1,000 a year in credit card interest alone, according to recent Federal Reserve data. That’s money vanishing into thin air, money that could fund a vacation or pad your savings. But here’s the contradiction—while credit cards offer convenience, their soaring interest rates trap millions in a cycle of debt. In this article, we’ll explore practical ideas to reduce credit card interest, helping you reclaim control and build a more secure financial future. Stick around, because by the end, you’ll have actionable steps to cut those costs and breathe easier.

My Unexpected Battle with Ballooning Bills

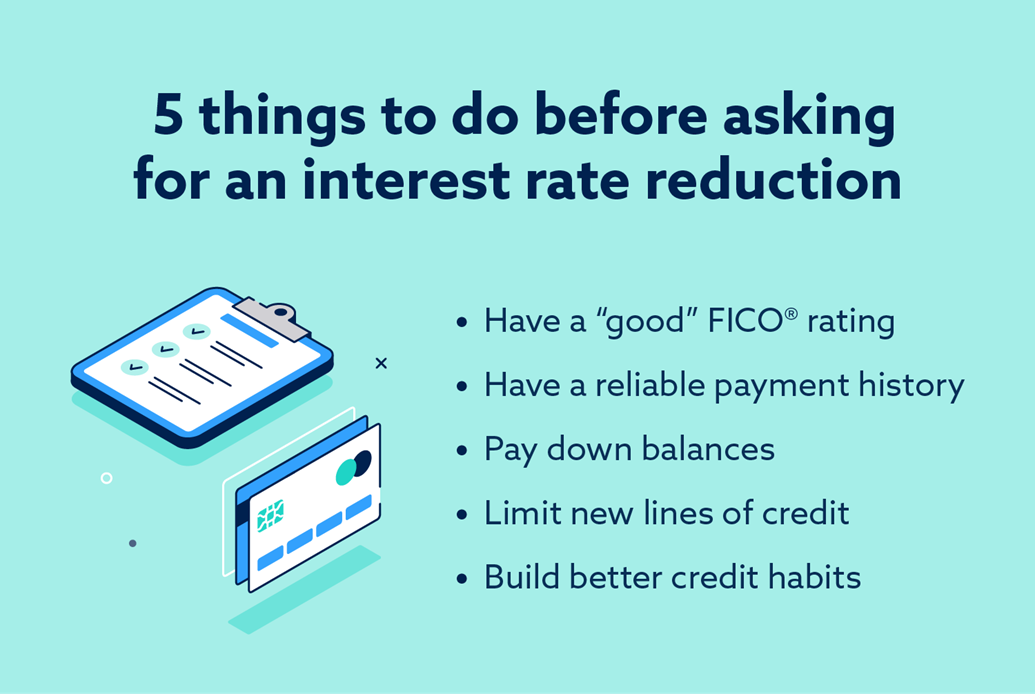

Back in 2015, I found myself knee-deep in credit card debt after a medical emergency hit my family hard. We’d racked up charges faster than a plot twist in a thriller movie—like something out of «Breaking Bad,» where one bad decision snowballs. I remember staring at my statement, thinking, «How did this happen?» The interest was climbing, turning a manageable balance into a monster. It was a wake-up call, teaching me that ignoring rates is like ignoring a leak in your roof; it only gets worse. Through that mess, I learned the value of proactive steps. For instance, negotiating with my issuer slashed my APR from 24% to 18%—a real game-changer. Reducing credit card interest isn’t just about numbers; it’s about regaining peace of mind, especially when life’s curveballs keep coming.

Let’s dive deeper. One effective strategy is balance transfer offers, which let you move debt to a card with a 0% introductory rate. I did this myself, and while it sounds straightforward, it’s not without pitfalls—like the transfer fees that can eat into savings. Still, for those with good credit, it’s a lifeline. And here’s a subjective take: in a country like the US, where consumerism is king, we’ve got to push back against the «buy now, pay later» mentality. Bite the bullet and call your provider; you might be surprised how often they budge, especially if you’re a loyal customer. That personal anecdote? It’s not just filler—it’s proof that lower interest rates on credit cards are within reach if you’re willing to ask.

Historical Echoes: What the 2008 Crash Teaches About Debt Management

Fast-forward to the Great Recession, and you’ll see echoes of today’s credit woes. Back then, families watched their interest rates skyrocket as the economy tanked, much like how inflation has nudged card APRs upward recently. It’s a stark comparison—think of it as a financial hurricane that exposed the fragility of unchecked borrowing. In the US, where the stock market crash wiped out trillions, folks learned the hard way that credit card debt strategies aren’t optional; they’re essential for survival. And just as policymakers pushed for reforms like the CARD Act to cap abusive practices, you can take cues from history to fortify your own finances.

Now, let’s get practical. Consider debt consolidation loans, which bundle your cards into one lower-interest payment. Compared to sticking with high-rate cards, this can save hundreds annually. To illustrate, here’s a simple table breaking down two common approaches:

| Strategy | Pros | Cons | Potential Savings* |

|---|---|---|---|

| Balance Transfer | 0% intro rate for 12-18 months | Transfer fees (3-5%) | Up to $500 on a $5,000 balance |

| Debt Consolidation Loan | Fixed lower rate (e.g., 7-10%) | Requires good credit | Up to $1,000 on the same balance |

*Estimates based on average rates; actual savings vary. This isn’t just theory; it’s drawn from post-recession trends where savvy borrowers cut their interest burdens by half. And that’s when it hit me—waiting for rates to drop is like waiting for a bus that never comes. Cut to the chase: by blending historical lessons with modern tools, you can craft a plan that fits your life, turning potential pitfalls into stepping stones.

The Overlooked Enemy: Minimum Payments and Your Escape Route

Ever feel like minimum payments are a trap designed to keep you hooked? They are, in a way—paying just the minimum on a $1,000 balance at 20% APR means you’d owe interest for years, stretching payments out forever. It’s ironic, really; what seems helpful ends up costing more. But let’s flip this on its head with a mini experiment: grab your latest statement and calculate how much extra you’d pay over time by only meeting the minimum. Go on, do it now—multiply your balance by the APR and divide by 12. Shocking, isn’t it? That exercise alone might push you toward paying more aggressively, which is key to reducing credit card interest effectively.

In my opinion, automating extra payments is underrated. Set up to pay double the minimum each month, and watch your balance shrink faster than expected. For those in debt-heavy regions like urban America, where living costs fuel card use, this is a game-changer. And here’s an unexpected analogy: managing interest is like pruning a garden—neglect it, and weeds take over, but tend to it regularly, and you reap the rewards. Remember, though, success isn’t instant; it’s about consistent effort, much like the grind in a classic finance flick, «The Wolf of Wall Street,» minus the excess. By confronting this enemy head-on, you’re not just saving money—you’re building resilience for whatever comes next.

And just like that, we’ve circled back to the bigger picture. What if reducing credit card interest wasn’t just about dollars, but about freeing your mind from financial worry? Take action today: review your cards, negotiate those rates, and start that extra payment plan. How has high interest rates shaped your financial journey—has it pushed you to innovate or simply survive? Share your thoughts in the comments; let’s keep the conversation going. After all, in the world of finance, we’re all in this together.