Money whispers secrets. In a financial world obsessed with high-risk, high-reward gambles, the humble high-interest CD stands as a quiet rebel, offering steady growth without the drama. Yet, here’s the uncomfortable truth: while stock markets soar and crash like rollercoasters, many folks miss out on the security of a certificate of deposit (CD) that could shield their savings from inflation’s bite. If you’re tired of watching your hard-earned cash languish in a low-yield account, this guide walks you through the essential steps for opening a high-interest CD, potentially earning you better returns with minimal effort. By the end, you’ll see how this straightforward move can bolster your financial stability, turning passive savings into a smart, reliable ally.

My First Stumble with CDs: A Lesson from the Brink

Picture this: back in 2012, I was a fresh graduate drowning in student loans, staring at a meager checking account that barely covered rent. I remember thinking, «Why not throw it all into stocks?» But then, a family friend—let’s call him Uncle Joe, the eternal optimist with a knack for conservative finance—sat me down over coffee and shared his own tale. Joe had opened his first high-interest CD during the dot-com bust, locking in a rate that outpaced inflation while the market tumbled. He lost nothing, while others scrambled. In my opinion, that’s the real beauty of CDs—they’re not flashy, but they’re dependable, like that old oak tree in your backyard that weathers every storm.

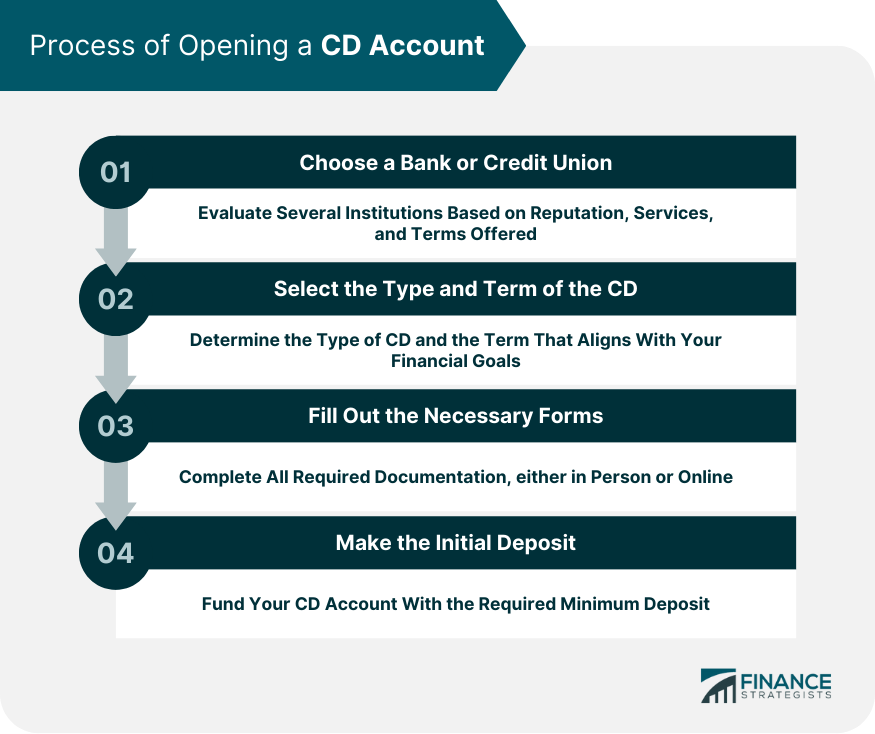

Fast forward to my own misstep: I dabbled in a short-term CD without reading the fine print, and boy, did I tie up funds when an emergency hit. Y justo ahí, when I needed liquidity most… It taught me a harsh lesson about terms and penalties. Joe’s story reinforced that understanding the basics isn’t just smart; it’s essential for anyone eyeing a certificate of deposit. So, if you’re on the fence, start by evaluating your timeline—aim for a CD that matches your goals, whether it’s a one-year term for flexibility or longer for compounded growth. This personal anecdote isn’t to scare you, but to ground you: finance isn’t about getting rich quick; it’s about building a foundation, one step at a time.

CDs Through the Ages: A Timely Financial Showdown

Ever wonder how today’s high-interest CD stacks up against the savings tools of yesteryear? Let’s rewind to the Great Depression, when banks introduced CDs as a safe haven amid chaos, much like how investors today flock to them during economic uncertainty. Back then, these instruments were a ballpark figure for stability, offering fixed rates that beat the erratic bond markets. Fast-forward to now, and we’re in a different era, with CDs competing against high-yield savings accounts and money market funds. Here’s where it gets interesting: unlike a savings account that fluctuates with Federal Reserve decisions, a CD locks in your rate, providing predictability that’s akin to planting seeds in fertile soil—they grow steadily, regardless of weather.

But don’t take my word for it; consider this cultural parallel. In the U.S., where «a penny saved is a penny earned» echoes Benjamin Franklin’s wisdom, CDs embody that frugal spirit, especially for Main Street investors wary of Wall Street’s volatility. Compare that to, say, the European approach with fixed deposits, which share similarities but often come with stricter regulations. A quick table might help clarify:

| Feature | High-Interest CD | High-Yield Savings Account |

|---|---|---|

| Interest Rate Stability | Fixed for term | Variable, can drop |

| Liquidity | Penalties for early withdrawal | Easy access anytime |

| Best For | Long-term savers seeking security | Emergency funds needing flexibility |

This isn’t just history; it’s a wake-up call. As inflation creeps up, like in the recent post-pandemic surge, a high-interest CD could outpace it, offering real growth. In my view, it’s less like betting on a horse race and more like a steady jog—reliable, if a bit unexciting.

Demystifying CD Myths: Your Personal Finance Experiment

What if I told you that the biggest barrier to opening a high-interest CD is often just misinformation? Let’s tackle a common myth head-on: «CDs are only for the wealthy.» Nonsense—anyone with a few hundred dollars can start, but here’s the twist: it’s not about hoarding cash; it’s about strategic placement. Imagine a conversation with a skeptical reader: «Sure, but what if rates drop while my money’s locked up?» I’d counter with this: rates are fixed at opening, so you’re protected, unlike with a fluctuating savings account. To make it real, try this mini experiment—grab your bank’s app or website right now and compare current CD rates to your existing savings yield. You’ll likely see a difference that adds up over time, especially with compounding interest.

This exercise isn’t theoretical; it’s practical, drawing from my own habit of reviewing rates quarterly. And here’s a subtle nod to pop culture: remember how Tony Stark in Iron Man always plans for the worst? That’s the CD mindset—preparing for uncertainty without overcomplicating things. The solution? Focus on steps like checking for FDIC insurance to ensure your investment is safe, then select a term that aligns with your goals. By confronting these myths with action, you’re not just saving; you’re investing in your future with eyes wide open.

In wrapping this up, here’s the twist: while we’ve focused on the mechanics, a high-interest CD isn’t just about numbers—it’s about reclaiming control in an unpredictable world. So, take the leap: research top banks for the best rates and open your CD today, starting with a simple online application. How will you adapt these steps to fit your unique financial journey? Share your thoughts in the comments; let’s build a community of savvy savers.