Shadows linger longer. That’s the uncomfortable truth about financial statements—they hide discrepancies in the dark corners of your records, waiting to trip you up. Did you know that according to a recent survey by the Association of Chartered Certified Accountants, nearly 30% of businesses uncover significant errors during routine audits? These mistakes aren’t just numbers on a page; they can lead to hefty fines, lost opportunities, or even business failure. But here’s the silver lining: by mastering the steps to audit your financial statements, you gain control, ensure accuracy, and pave the way for smarter financial decisions. In this article, I’ll walk you through a practical process, drawing from my own experiences, to help you audit like a pro and safeguard your financial health.

My Wake-Up Call with Financial Blunders

Picture this: a few years back, I was running a small consulting firm in the bustling streets of New York, thinking I had everything under control. My financial statements looked neat on the surface, but oh boy, was I wrong. It was during a routine tax season when I decided to dig deeper—something I now call my personal audit awakening. I found duplicate entries in my expense logs that inflated costs by thousands, all because I hadn’t cross-verified my bank statements with receipts. I remember thinking, «This can’t be happening,» as I stared at the mess. That experience taught me a hard lesson: auditing isn’t just a chore; it’s a lifeline. In my opinion, skipping it is like ignoring a ticking time bomb under your desk.

To start auditing your financial statements effectively, begin with gathering all your documents. This means pulling together your balance sheets, income statements, and cash flow reports from the past year. Use tools like QuickBooks or Excel for organization—keywords like «financial audit process» often highlight how these can streamline the task. A metaphor I’ve come to love: think of it as sifting through a detective’s case file, where every receipt is a clue. And just there, in the midst of the chaos, I realized how one overlooked detail can snowball into a bigger problem. By sharing this, I’m not just listing steps; I’m urging you to see the human side of finance, where real mistakes lead to real growth.

From Ancient Ledgers to Modern Spreadsheets: A Timeless Comparison

Fast-forward from the clay tablets of ancient Mesopotamia, where merchants etched their transactions, to today’s digital dashboards—auditing financial statements has evolved, but the core principles remain strikingly similar. Back in the day, a simple error in a ledger could mean the difference between prosperity and ruin, much like how a misentered figure in your current ERP system might break the bank today. I find it ironic that while technology promises perfection, human error persists; a study from Deloitte shows that 40% of audit failures stem from input mistakes. In the U.S., where I’m based, this cultural reliance on tech sometimes blinds us to the need for manual checks—think of it as trusting your GPS without ever glancing at a map.

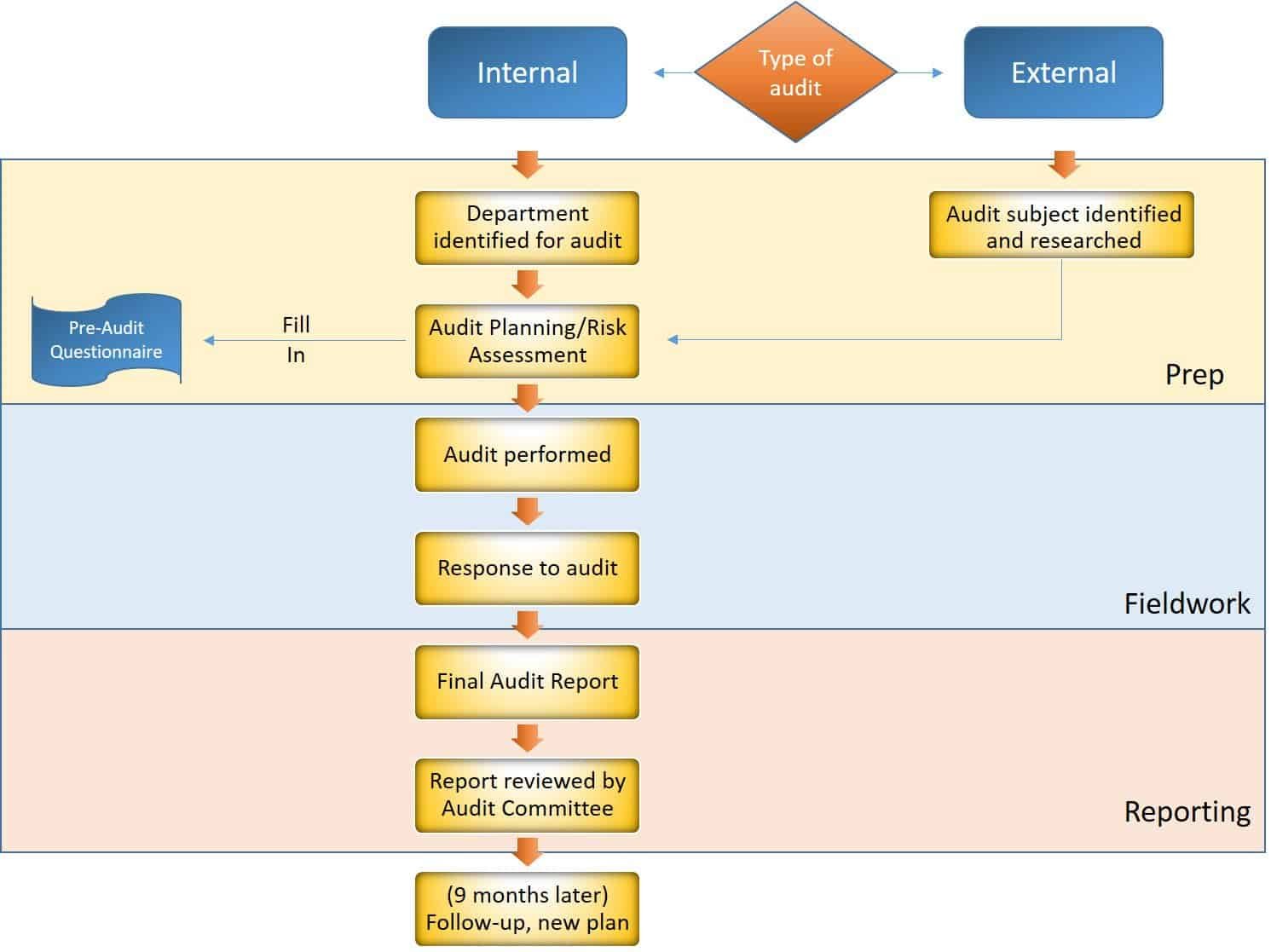

Now, let’s compare two approaches: traditional manual audits versus automated software. For instance, a manual audit involves physically verifying each entry, which is thorough but time-consuming, while tools like Xero offer real-time automated financial reviews that flag anomalies instantly. Here’s a simple table to illustrate:

| Aspect | Manual Audit | Automated Audit |

|---|---|---|

| Time Required | High (days or weeks) | Low (hours) |

| Accuracy | Depends on human diligence | High, with algorithms |

| Cost | Labor-intensive, potentially expensive | Affordable subscriptions |

| Advantages | Deep insight into details | Speed and error detection |

This comparison isn’t just academic; it’s a wake-up call to blend both for optimal results. Personally, I’ve adopted a hybrid method, and it’s on the money every time. Remember, auditing your statements is about historical accuracy meeting modern efficiency—much like how «The Godfather» films blend old-school storytelling with timeless themes.

The Hidden Pitfalls in Your Statements – And How to Dodge Them with Strategy

Ever wondered why that «minor» discrepancy in your revenue forecast keeps nagging at you? It’s because financial statements are riddled with potential traps, from understated liabilities to overinflated assets, and ignoring them is like walking a tightrope without a net. In finance circles, I’ve heard experts quip that these errors are the «ghosts in the machine,» subtly undermining your business’s stability. Drawing from my earlier blunder, I once overlooked a deferred tax liability, which nearly derailed a loan application. The solution? Implement a step-by-step verification process that targets these vulnerabilities.

First, scrutinize your income statement for revenue recognition issues—ensure all sales are recorded in the correct period. Then, 2. Dive into the balance sheet, checking for accurate asset valuations; assets can depreciate faster than you think. 3. Finally, reconcile your cash flow statement with bank records to catch any cash leaks. This structured approach, often searched as «steps to audit finances,» transforms a daunting task into manageable wins. And here’s a twist: while software helps, your intuition—honed from real-world experience—is the secret weapon. I believe that by addressing these pitfalls head-on, you’re not just fixing errors; you’re building resilience, much like a fortress against economic storms.

In wrapping this up, auditing your financial statements isn’t merely about compliance—it’s a path to empowerment, revealing truths that can reshape your financial future. Think of it as flipping the script: what if those hidden errors were actually hidden opportunities? So, take action now—grab your statements and run a quick spot-check using the steps we’ve covered. Y’know, just to be sure. And here’s a question to ponder: What financial ghost might be lurking in your own records, waiting to be exorcised? Share your thoughts in the comments; let’s turn audits into conversations.