Wealth hides in plain sight, often overlooked by those chasing get-rich-quick schemes. Here’s a stark truth: according to a study by Ramsey Solutions, 79% of millionaires didn’t inherit their fortune—they built it through disciplined, everyday strategies. Yet, in a world buzzing with financial jargon, many feel lost at the basics, wondering how to turn a modest income into lasting security. This article cuts through the noise, offering **serious strategies for wealth building basics** that can empower you to take control, build a solid financial foundation, and achieve independence without the hype.

My Journey from Debt to Stability

Picture this: back in 2008, when the economy tanked like a scene from «The Big Short,» I was drowning in credit card debt, barely scraping by as a young professional. It wasn’t pretty—I’d splurge on dinners out, thinking it was my reward for long hours, only to wake up to bills that wouldn’t quit. But that low point forced a change. I started tracking every dollar, a simple habit that shifted my perspective. And that’s when it hit me, right in the wallet: wealth isn’t about earning more; it’s about managing what you have.

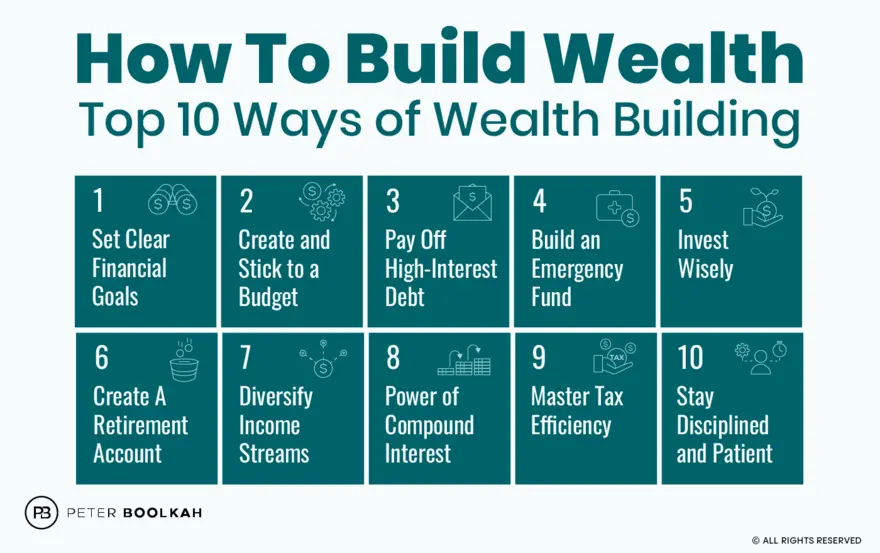

In my opinion, based on years of trial and error, the cornerstone of wealth building is budgeting. It’s not glamorous, but it’s effective. Think of it as planting seeds in a garden—neglect it, and weeds take over. I adopted the 50/30/20 rule, allocating 50% of my income to needs, 30% to wants, and 20% to savings and debt repayment. This **basic finance tip** isn’t just theory; it worked for me, turning my chaotic finances into a nest egg that grew over time. Across the pond in the UK, folks call this «making ends meet,» but here in the US, it’s about that American dream of self-reliance. Sure, it sounds straightforward, but skipping this step is like trying to build a house on sand—inevitably, it crumbles.

Lessons from History’s Wealth Builders

Fast-forward to ancient times, and you’ll find that the **strategies for wealth building basics** aren’t new. Take the Medici family in Renaissance Italy; they didn’t just paint pretty pictures—they mastered banking and diversified investments, turning Florence into a financial hub. Compare that to today’s gig economy, where side hustles mimic their entrepreneurial spirit. It’s a cultural parallel: just as the Medicis invested in art and trade for long-term gains, modern folks can apply this by diversifying portfolios, blending stocks with real estate.

But here’s an unexpected analogy: building wealth is like crafting a symphony, where each instrument—saving, investing, and debt management—plays its part. In the US, we often reference «pulling yourself up by your bootstraps,» a modism that underscores self-made success, but it’s more nuanced. Historical figures like Benjamin Franklin preached frugality, saving «not for the sake of saving, but for the sake of spending wisely.» This contrasts with common myths, like the idea that wealth is luck-based. The uncomfortable truth? Only 10% of millionaires attribute their success to inheritance, per the same Ramsey study. By emulating these lessons, you’re not just saving money; you’re creating a legacy, much like how Franklin’s Poor Richard’s Almanack still echoes in financial advice today.

| Investment Type | Potential Returns | Risk Level | Best For |

|---|---|---|---|

| Savings Accounts | 1-2% annually | Low | Emergency funds and short-term goals |

| Stocks | 7-10% historically | High | Long-term growth and wealth accumulation |

| Real Estate | 8-12% with appreciation | Medium | Passive income and diversification |

Demystifying the Math Behind Steady Growth

What if I told you that compound interest is the silent hero of wealth building, yet so many overlook it? It’s like watching a snowball roll downhill—starts small, but gains momentum. In my experience, ignoring this basic principle cost me years of potential growth. Here’s a disruptive question: why do people chase high-risk investments when a simple 401(k) could double their money over decades? The answer lies in education, not luck.

To counter this, let’s break it down: start with an emergency fund covering 3-6 months of expenses—that’s step one, ensuring you’re not derailed by life’s curveballs. Step two, automate investments; it’s like setting a course on autopilot. And three, diversify to mitigate risks, drawing from that historical wisdom we discussed. In American culture, we say «don’t put all your eggs in one basket,» and it’s spot-on for finance. The irony? Many think wealth building requires genius-level smarts, but as Warren Buffett, a pop culture icon in finance, puts it, «The most important quality for an investor is temperament, not intellect.» So, by applying these **wealth building strategies**, you’re not just avoiding pitfalls; you’re paving a path to financial freedom.

In wrapping this up, here’s a twist: the real secret to wealth isn’t in the strategies themselves, but in your commitment to them over time. It’s not about becoming the next Buffett overnight; it’s about small, consistent actions that compound. So, take this actionable step: review your budget today and allocate just 10% more to savings. And what about you—what overlooked habit will you tweak to start your wealth journey? Your comments could spark real change for others.